Restructuring GB’s Energy Institutions – why it is worth the cost

Catherine Mitchell, IGov Team, 18 April 2016

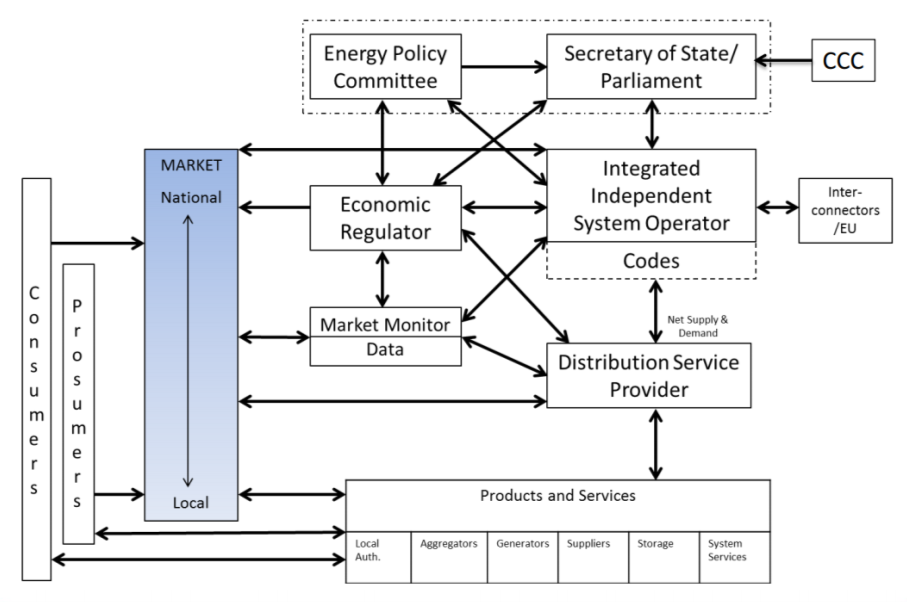

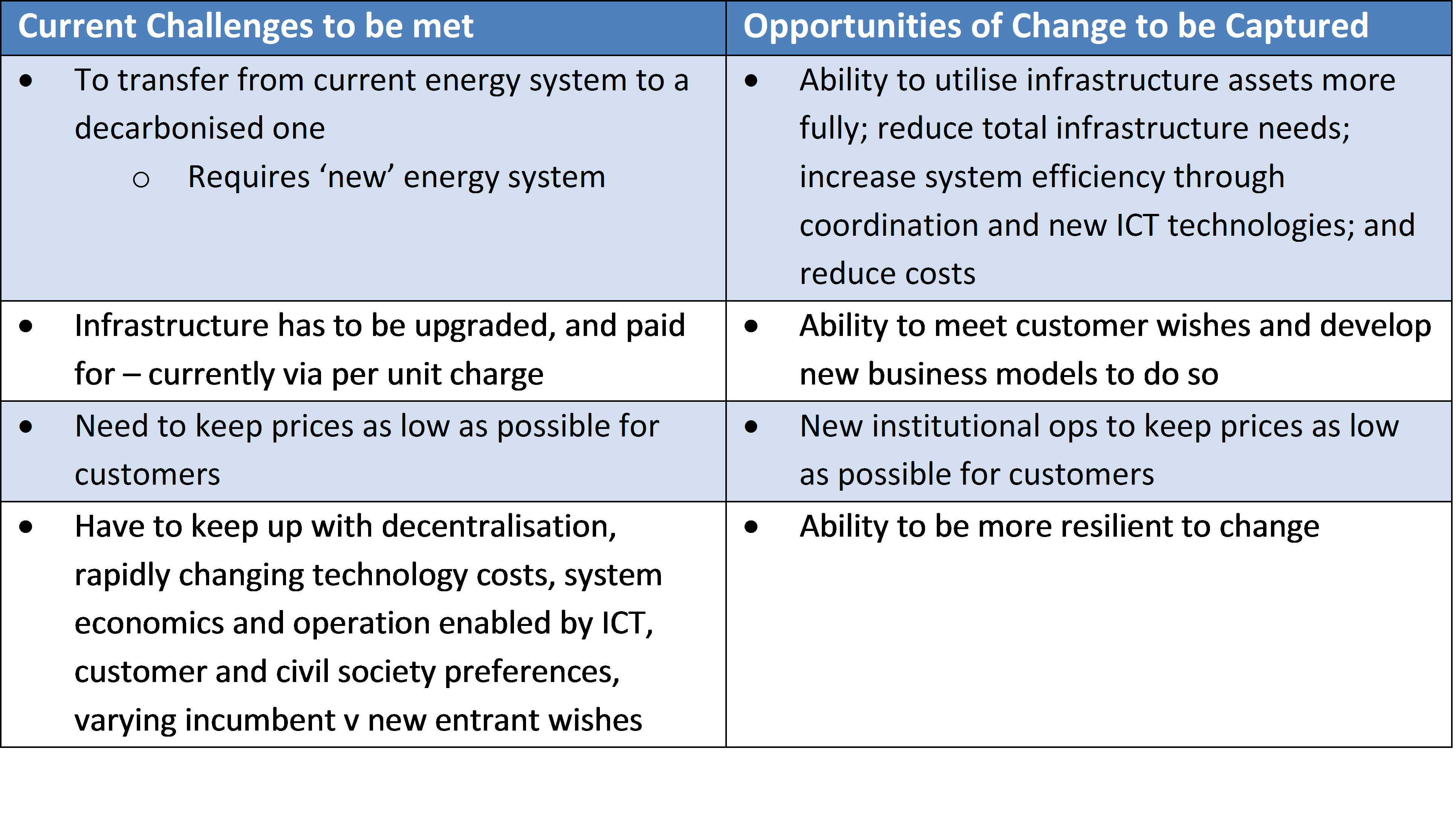

IGov has been advocating an institutional framework (see Figure 1) which it argues will better meet the challenges faced by the GB energy system, whilst also opening up new opportunities and enabling their capture (Table 1 at the end). However, from the point of DECC and the Minister, one can understand if they ask: what is the cost of this, and is it worth the effort? We argue that we cannot know what the true ‘total’ benefits would be in terms of money, but there are reasons for thinking that they would be very large, as set out below. The framework would open up, rather than close down, the opportunities presented by an increasingly decentralised energy world. Moreover, the costs of the counterfactual – keeping going with an increasingly not-fit-for purpose governance – are also uncertain, and certainly large.

The basic framework (Figure 1) that IGov argues for is: more direct accountability for energy policy to the Minister; an advisory / executive body which works to the Minister, which we have called an Energy Policy Committee (EPC) because we see it as quite small and nimble, and which has hierarchy over the other energy institutions; an economic regulator, which should be pared back from Ofgem; an independent and integrated System Operator (IISO), which includes the national wholesale market operations and Code Administration; distribution service providers (DSPs) which manage local markets; a market monitor and a data body. This is broadly a cherry-picked combination of the Danish and NY State regulatory system.

Figure 1 Proposed IGov Institutional Framework

It may seem like a lot of changes, and certainly the roles of most actors would change (we describe this in a submission on strategic policy statements to DECC). However, institutionally, the basic steps and timelines needed to make the framework changes are reasonably straight forward, even if the details might be more contentious. Creating an IISO is different from the other institutional reorganisations because the current SO is in the private sector. Stated baldly, the current SO effectively needs to be re-nationalised to become a State-owned not-for-profit IISO, and therefore NG would require compensation. We argue that the IISO would be more effective if it was working in conjunction with DSPs. [The costs of transferring DNOs to DSPs are mainly internalised in the transfer from RIIO to a nearly wholly performance based regulatory system, but these are minimal in the short term and expected to lead to substantial cost reductions over the medium term].

The first step is creating the EPC, the IISO, the economic regulator, the market monitor and the data body. The second step would be transferring the DNOs to DSPs and altering the market arrangements to enable linked local and national markets. All of this is dealt with in some detail on the IGov website via Working Papers, blogs and so on.

But would the outcomes be worth the effort and cost of the changes? The RIIO Electricity Transmission Annual Report 2014-15 has the SO’s asset value at £127m in 2015 , and presumably that would be about ball park that a new body would have to pay for it. This blog does not comment on whether this is the cost of creating an IISO – but, conceptually, were it to be in this ballpark: Would this be a good use of public money? We definitely think so, providing, as set out in a recent blog, that the new IISO is a state owned, not for profit entity, entirely separated from National Grid.

There are multiple reasons for this:

As the recent blog argued, amongst other conflicts of interests, the profits from the TO business relative to the SO are huge (£849 million in 2011/12 compared to £9 million), clearly weighting National Grid’s own incentive towards a more traditional transmission dominated energy system. This is worrying given that the energy world is decentralising, not just because of small scale supply technologies but also because of social preferences and the arrival (and expansion) of ICT to energy, for example here. That means that the active ‘heart’ of the energy system is rapidly moving to distribution, and the SO has to be in the position where it wholeheartedly embraces the new means, and economics, of system operation.

One important aspect of speeding up the process is the creation of an independent and integrated system operator (IISO) which delivers the EPC’s recommendations, based on the Committee on Climate Change’s carbon budgets, and which has technical expertise and knowledge (unlike DECC or the Economic Regulator) to manage the efficient operation of the national system. The IISO should be given responsibility from the Minister to maintain system security and to enable the transformation. The IISO needs to abandon the old separation between transmission and distribution, and embrace managing and balancing the whole, integrated system which includes local generation, storage and demand management etc via the distribution service provider platform (and here) but also by other flexibility means, such as interconnection with other countries. At the same time, both transport and heat are likely to become more integrated into the electricity system. The future of the electricity system is bound up with the future use of gas, and the gas network. The evolution of electricity, heat and transport should not only be thought about together, but also the operation of the systems should fit together, as should its regulation – hence our support for an Integrated and Independent IISO. The IISO acts as the conductor of the GB energy system orchestra to reach the recommended technical transformation on time, securely, and cost effectively. Again, there is value in this overarching, managerial integrated system role.

The IISO therefore has a very important overseeing and management role. It is the co-ordinator of the energy system – this includes the TO, the DSPs as well as the interconnectors and markets. The argument put forward by the NY REV is that if DNOs are transformed into DSPs and regulated primarily by performance based regulation then whilst the DSPs can make a higher rate of return on their PBR portion of revenue, the overall cost to customers of total infrastructure and distribution system management will be lower, whilst at the same time improving customer service and better enabling the meeting of energy policy goals. No hard estimates are currently available, but the final agreement for the timeline of transformation from DNO to DSP and its regulatory basis is due in May 2016. If one assumes the projected reduced total costs would also be the case in GB, then an IISO is vital to unlocking those savings and for managing the 14 or so DSPs, and that alone appears to far outweigh the costs of moving to an IISO.

Moreover, because the energy system is decentralizing – whether in terms of supply technologies, ICT operation and sensor technologies, ownership, prosumers, new entrants, new services and so on – and because energy demand is always local – efficient utilization of assets and resources and coordinated energy management best occurs at the distribution level. It simply is not possible for this to occur at the national level because efficient system operation with new technologies relies on an intimate knowledge of the energy system which is to be coordinated. Distribution coordination makes sense because of scale. The IISO provides the necessary system oversight, whilst the DSPs run the systems efficiently as market facilitators. The IISO and the DSPs are two sides of the same coin – but hierarchy of decision-making has to be with the IISO because of its system responsibility. Establishing trust within the energy system actors is vital, and that hierarchy would not easily be given to the SO by the DSPs if the SO remained linked to National Grid.

There are costs in continuing as we are, although also unknowable. The counterfactual to the IISO is a situation where current arrangements are maintained and where costs are likely to increase as that ‘old’ system becomes increasingly unfit for purpose in an increasingly decentralised context. The counterfactual of not having locally competent DSPs is likely to be constrained investment and innovation by local communities/Local Authorities/cities, as well as all the costs around under-utilised assets, reducing the cost of maintaining security etc which are part of the fundamental reason to support IISO/DSP and a more co-ordinated system. This also includes our ability as a nation to play a leading role in rapidly expanding markets (in storage, DSR, efficiency, ITC), opportunities around which can be expected to increase under IISO / DSP arrangements.

Furthermore, it is important to note that developing innovative smart grid solutions, particularly in the area of demand-side response, may potentially present a significant opportunity for GB, not only to respond to domestic system integration challenges, but also to provide leadership at the international level in novel smart grid applications, advanced data and system management and novel business models. For example, successful deployment of DSR in the UK may create valuable know-how expertise in an area which will be in high demand worldwide in the coming decades. Strbac et al, NIC 2016

Moreover, there is increasing support for communities / local areas to retain the energy economies within their local area. The Wadebridge Renewable Energy Network argues that the Wadebridge, a small market town in Cornwall, energy economy is probably worth about £13 million pounds a year. They argue the greater proportion of that retained within Wadebridge the better for Wadebridge, and have set up an energy company to do that. Bigger centres, for example, Bristol support the same argument, albeit with greater value to their energy economy. Again, this should have a value to be included in the calculation of whether the creation of an IISO is worth the cost, which would make it easier for these sorts of initiatives to thrive.

Standard economic analyses are poor when comparing the economics of one regulatory system which is in place versus another regulatory system which could be in place, because it is impossible to understand the structural and dynamic impacts of change going in to the future. Undertaking an analysis of the current governance system versus the IGov framework is therefore essentially unknowable. Nevertheless, maintaining the current top-down, centralized, mainly passive operating system will lead to GB slowly but surely diverging from the momentum of the global energy system. At some point, that divergence will be so great that eventually a decision-maker will say: why do we run our systems like this? Why are our system costs so great relative to other countries, and our efficiency so poor? In this situation, there is likely to be substantial political and innovation costs to maintaining a BAU approach to energy policy. Far more cost-effective to follow through with a reset now.

The bottom line however is that the current GB energy system relies heavily on expensive subsidies rather than markets. This is fundamentally because GB’s energy policy has tried to apply ‘old’ solutions to the current challenges of the energy system – but spending money to patch up the system has not successfully dealt with those challenges. For example fossil fuel and nuclear power are displaced from electricity markets by variable power, and peak prices come down thereby reducing fossil and nuclear profits. GB’s answer to that – instead of saying ‘great, this is showing that our 25 year sustainable energy policy is beginning to work’ – has been to establish a subsidized capacity market (which keeps fossil fuels going) and to sharpen cash out prices. Neither do anything in terms of moving the electricity market away from subsidies and back to a market which fits with the needs of a sustainable, secure, decentralizing energy system.

If GB is to move back to energy markets it has to meet the current challenges of the electricity system and open up space for the new opportunities (see Table 1 below) and IGov argues the way to do that is the IGov framework including the combo of an IISO, DSPs as market facilitation platforms for services and local markets. Subsidies may still be needed for some resources, but the cost of those subsidies will be considerably lower than those going to the current set of technologies. Thus, this ‘straw’ cost of £127 m to establish an IISO seems cheap relative to the current capacity market alone, which is costing us £1bn a year, never mind the cost of other technology subsidies and not including the benefits of better system operation, including integrating with heat and mobility, and distribution markets. Overall, therefore, moving to an IISO seems to make good economic sense. Just as importantly, it is also a vital and important dimension of the transformation to an institutional framework capable of cost effectively orchestrating the move to a sustainable, secure and affordable energy system.

Posted by: rhoggett

Related Posts

« Previous New Thinking: Distribution Service Providers Presentation: Energy Transformation Next »

{kind=link}