Energy Distribution Service Providers – another piece of the governance puzzle

Catherine Mitchell, IGov Team, 8th January 2016

IGov is exploring the link between innovation and energy governance, where governance is taken to be policies, institutions, rules and incentives. We are interested not only in these policies, institutions and rules and incentives – but how they develop – the politics behind their creation and implementation. IGov is putting together a framework for energy governance suitable for the 21st Century. This includes arguments for the restructuring, or creation, of institutions and the altering of rules and incentives within the GB energy system – and we are provisionally calling this Output Based Regulation. Our latest addition to this framework was our recommendations for Code Governance reform (see page 44 for figure), which includes our argument to get rid of self-regulation of codes.

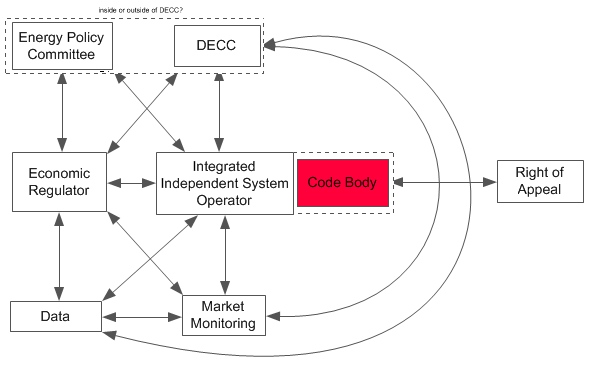

The energy world is changing rapidly and it is clear that current GB energy governance is no longer fit for purpose. We argue (as shown in Figure 1) that the roles and relationships between the GB energy institutions need to change – hence the need for: an energy policy committee (EPC); an integrated and independent system operator (IISO) which is the body tasked with transformation and ensuring security and which combines complementary market and network functions; that Ofgem be restructured so that it becomes an economic regulator, and that it is on the same level of hierarchy as the IISO. We think the IISO and the Economic Regulator should be overseen by the EPC which both advises the Secretary of State but also executes the Secretary of States decisions, thereby bringing in more legitimacy to decision-making.

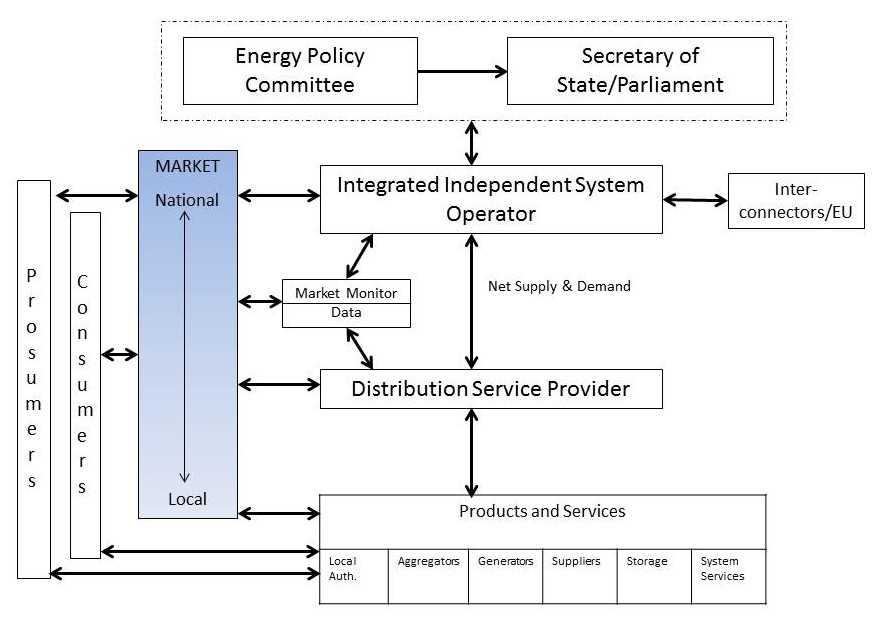

This blog introduces the potential of distribution service providers (DSPs) to be the ‘heart’ of the energy system (as shown in Figure 2). It is a straw proposal intended to enable discussion, and we welcome comments.

In the near future, we will set out our arguments for a new electricity market design suitable for an energy system with high proportions of variable power, and which also includes the demand side. We will also set out our views on aggregation; the retail market; a Data Body; and the importance of market monitors.

Figure 1

Distribution Service Providers

IGov has argued that we in GB need a publicly owned system operator (the IISO). This body would be made responsible for security and transformation to whatever energy system is suitable for meeting the CCC’s recommendations. This IISO is a System Operator in the sense that it is overseeing the most efficient operation and development of both transmission and distribution. It is also independent in the sense of being a publicly owned not for profit entity, and it is integrated because it would link electricity and heat, and oversee local through to national market operation.

In the same way that we think the transmission system operator role needs to be transformed, we think distribution network operators (DNO) should also alter their role. We think that this is best done by means of new regulation which alters the incentives received by the DNO. Transforming DNOs into market facilitators has been discussed as far back as the Embedded Generation Working Group in January 2001. Currently, there is a spectrum of possible roles that the DNOs can transform into – and these options need to be discussed fully.

At one end, the minimal change is that DNOs are regulated in a different way from currently. At the other end, DNOs are transformed into Distribution Service Providers, as envisaged in the NY REV, which facilitate fully formed local markets for energy. Somewhere in the middle, are DNOs transformed into distribution service providers / market facilitators but where local markets, if they exist, are ad hoc arrangements which buy and sell into a national market. It seems to us that DNOs need to transform. We also like the idea of local markets because of the arguments put forward by the NY REV (discussed below) and because of the (already) increasing interest from places of different sizes in GB to develop local markets (eg Bristol and Wadebridge).

Figure 2 below sets out how we see the transformed distribution service provider interacting with other energy institutions such as the IISO, markets, customers, data and so on. Please also see Figure 1 for how this fits into the IGov governance framework which has been developed so far.

Figure 2

There are 5 key points about transforming DNOs:

- What would a DSP do, and why is it preferable to the current DNO?

- Would the transformed DNOs remain private companies or would they (or some part of them) become state owned (or indeed community owned)?

- How would the distribution level local markets be incorporated into national or regional markets?

- What is the relationship between the SO and the DSPs?

- What does this mean for data accessibility and market monitoring?

What would a DSP do, and why is it preferable to the current DNO?

Within the NY REV, there is the new value proposition of Distribution Service Provision. In effect, the DSPs manage local energy markets (which effectively net off supply and demand as far as is cost-effective at the local level) and network development to suit customer focused products and services (ie to make sure that customers are able to connect photovoltaic cells, participate in demand side response programs or have an electric vehicle charger) and to fulfil public interest goals, such as the move to a decarbonised energy system. While, the DSP is, in one sense, a local system balancer, this is only one part of its role which is also to be: a market facilitator for products and services and as a provider of data to enable new products and services for the benefits of customers. In addition, an efficient, customer focused energy system must be able to be operated efficiently at the local level – because this is the only way to fully integrate the demand side into the moment by moment, day by day operation of the energy system. The NY REV has chosen the distribution level as the central energy market facilitator because of this unique ability to bring all these capabilities together, potentially connect customers to their energy use, and to capture a greater efficiency of energy use by reducing losses and so on.

Moreover, within NY State the DSP is regulated – not just to maintain the network securely and to pass units of electricity or gas across it as is currently the case – but to encourage its performance as a market facilitator to meet customer wishes but also to meet public interest goals most affordably. This fits with our view that the effectiveness of regulation should be assessed on outputs.

Elsewhere, IGov has complained of a lack of flexibility in Ofgem because of its multiple tasks, and we have argued that the various tasks should be separated out. A DSP is different however. At the moment, the DNO basically passes energy across its networks in return for a payment. It may know if there is a problem somewhere on its network, and it may ask Ofgem for money in the next price control to rectify it. A great deal of money has been spent trying to encourage more innovative operation in distribution networks to limited effect. The problem has been that different actors have had no central way to access the possibilities at the distribution level because either data has been held by customers, suppliers or the DNOs, or because the DNOs control what happens on their networks. The DSP, by bringing these actors together along with the enabling factors, such as data, make this possible.

Would the transformed DNOs remain private companies or would they (or some part of them) become state owned?

The IISO is envisaged as guiding energy system development (both transmission and distribution) to meet 2050 needs, and the targets between now and then; and to establish a way to value system capabilities (including but not only energy) in a market which is complementary to system operation and development. We argue that the IISO should be state-owned – rather like energienet in Denmark. One question for GB is whether a DNO which is transformed into being a market facilitator or service provider should continue as a private company or whether they should also become state/ municipal/locally owned – as occurs in different ways in different countries.

How would the distribution level local markets be incorporated into national or regional markets?

The EU currently has a consultation on electricity market design, and individual Member States are working out their preferences for how their own markets are designed, including how they interconnect with other countries (eg Germany) and how they value the multitude of capabilities needed to keep an energy system running securely. Nordpool and the Pentalateral Market are good examples of markets which cover several countries and where individual country or sub-national markets fits into the bigger cross-country market. It seems to us that local markets should be able to do the same within the national country markets without technical problems, providing the market is designed to do so.

An electricity market, suitable for a sustainable, secure and affordable energy system, has, conceptually, to integrate a national energy system level market with more local involvement. We can envisage a situation where actors, as shown in Figure 2, are able to choose whether they sell into / buy from a local market or directly from /into the national market. The point is that it is one market which has design features to enable local involvement, and probably multi-country involvement as well. This requires a new market design, and it requires a new means of data availability. This market design – based on complementary national and local markets and system operation – will be described in detail a future blog. Figure 2 shows however the basic framework.

The combined (current) rules and incentives of balancing; the means to pay for networks; and the buying and selling of energy itself in markets combines to create an investment climate for different actors and products. The DSP is a new ‘platform’ to buy and sell products and services in a ‘new’ place. The local market is a central dimension of the DSP. In this way, the argument is, that it opens up new opportunities which should lead to a more efficient energy system – whether it be cheaper because less infrastructure kit is required; whether it be more environmental because value can be given to particular technologies or habits; or whether it be more secure as a result of its diversity and resilience. The degree to which this is the case in practice has yet to be tested – although there is a Brooklyn Queens Pilot, a $200 million project.

What is the relationship between the SO and the DSPs?

Another important area of regulatory clarity is the extent to which the DSPs have autonomy from the SO. We envisage the IISO establishing the vision to 2050, and steering the system development towards that. The economic regulator would then regulate the networks based on that. The idea of an IISO is that it avoids the competition between transmission and distribution and moves to an institution which should be focused on flexible, efficient system operation. The DSP should bring benefits by revealing the value of the demand side at different times and places at the distribution level; the value of different products and services at the distribution level, including the demand side, to customers. Understanding this value should then lead to more efficient investment and improved system costs as well as stimulating value related tariffs based on time, location, and services. The idea is that DSPs are regulated to encourage outcomes which fit with the IISO vision – ie traditional goals, such as resilience; but also environmental goals, such as CHP or renewables and the demand side; and then goals related to the new business models or public interest concerns. In this sense, DSPs are autonomous but they are directly working with the IISO vision.

What does this mean for data accessibility and market monitoring?

There have been concerns about the lack of market monitoring and the level of profit made within both GB markets and networks. IGov has argued that market monitoring is a vital dimension of a competitive energy system. We envisage the market monitor having access to IISO, DSP and market data.

We also envisage more transparency of data. Currently, customer data resides with suppliers. Customers can give permission to another company to access their data but this establishes a de facto barrier to widespread accessibility of energy data. Moreover because of the privatised nature of the GB energy system, one street or area will be supplied by multiple companies and it becomes very difficult to know what total energy use an area might use, or when, or whether it could in some way be shifted at certain times and so on.

The DNOs currently ‘know’ of problem areas in their network but providing a solution to them is within the cumbersome price control review and is not opened up to new actors. This improved transparency of data is at the heart of reforming energy governance. The issues are complex but GB will need to overcome them. One potential example is the DataHub in Denmark. We imagine this will require a firm step to another process. As with Codes, where the process of self regulation itself creates the central problem of Codes, so the problem of data is the current process. As with Codes, where self-regulation has to go, data collection has to be fundamentally altered.

Conclusion

Although our thinking with respect to DSPs is not finalised, we are clear that the role and regulation of DNOs has to change. It seems to us that DNOs can transform into exciting new institutions which can be a major force for reducing total energy use; for using energy more efficiently; for involving customers more in energy decisions; and for enabling more non traditional business models to become involved.

We would welcome feedback on this initial thinking: igov@exeter.ac.uk

Posted by: rhoggett

Related Posts

« Previous Paper: Governing for sustainable energy system change Submission: National Infrastructure Commission call for Evidence Next »

{kind=link}

One Response to: New Thinking: Energy Distribution Service Providers