Name, Form and Function of Distribution Entities – clarity and agreement needed across the world

Name, Form and Function of Distribution Entities – clarity and agreement needed across the world

Catherine Mitchell – IGov Team, 19th October 2018

The need for the traditional 3 part utility function of planning, operations and market administration broadly continues within the distribution area, even in this changing energy world, but changing technology, public policy goals, user preferences and business models are challenging whether the traditional distribution utility should still be responsible for each segment; whether the traditional role for the utility within those segments is also still necessary; and whether there are new functions (for example, local market coordination and balancing) which some entity needs to take on.

A few months ago I wrote a blog which argued that it did not matter whether we call the emerging distribution entity a DSO (distribution system operator or distribution system orchestrator (the latter a Navigant name) or a DSP (a NY REV distribution system provider (which originally came from Distribution System Platform Provider)) or a distribution service provider (DSP, IGov, and others)) – what mattered was the function of that entity.

However, I have now come to the conclusion that this laissez faire attitude above is unhelpful. We are moving to a world where the 3 traditional linked roles of the distribution entity may divide into new separate entities. In this world, we need to be clear about the names and functions of each distribution entity.

There are very few places around the world which are taking these steps. It is sensible that we learn from each other. Learning is made harder when there is little agreement on the names we are using for each entity, or their functions.

This is a 2 part blog. This Blog 1 sets out the potential differences in names and function, incorporating an interesting set of ideas from a 4 part Blog by James McGuiness from NYS. His blog ideas have many parallels to the IGov Vision, but he uses different names for the distribution entities, and his vision clearly derives from (or at least complements) his company interests. The differences in US and GB regulation also mean that the blog arguments are not entirely relevant for GB – and he certainly has ideas which would seem odd to us in GB – but overall he is introducing new ideas into the distribution governance debate, and he is critical of the type of change and rate of change so far in the NY REV. In the spirit of discussion, IGov is highlighting his ideas.

Blog 2 is simply a brief review of each of the blogs in the McGuiness 4 blog series – so any mistakes in its translation are all mine, and I apologise beforehand.

This blog is set out in the following way:

- A context (this repeats my definition (up until this point) of a DSO or DSP, given in a recent blog)

- It then argues that the understanding of distribution entities form and function has moved on from that blog, even though only a few months old, and explains how

- It introduces a blog series and its key ideas by James McGuiness from NYS, US

- It then asks what all this means for the names, functions and form of distribution entities in GB

- And then concludes

Context

The blog I wrote a few months ago, very briefly set out the different functions, as I envisaged them, of the DSO and DSP entities. I reproduce a few paragraphs below (square brackets are added from this blog to add clarity):

‘Of course, ultimately it is not the name (DSO or DSP) that matters but the functions and how they are regulated. I would, broadly, argue that the difference in function between a DSO and a DSP is that the former retains more control of the development and operation of the network because:

- there is a higher proportion of their revenues deriving from [undertaking the development, maintenance and operation work]* via cost of service inputs [to the price control]*;

- [by having control]* over which system service project to encourage (such as provisions to reduce constraints [and usually undertaken by 3rd Parties]*) but usually at the higher kVs than at the residential kV level;

- and does not undertake a coordinating and balancing market role for distributed electricity – so only deals with system service type markets rather than energy markets.

This is more active than the current passive distribution network operator (DNO) but not very much.

A distribution service provider on the other hand

- operates a coordinating and balancing market for electricity under grid supply points [ie area based]*, which are nested into the wholesale market;

- they act as a market facilitator and coordinator of non-distribution entity private platforms, and of area based energy and system services;

- it is incentivised to enable new transactions, in part by opening up data about the system operation and revealing price (through distributed energy resource (DER) assessments [in the distribution entity area]*;

- they are incentivised more directly to deliver public policy goals;

- they are incentivised to enable customer wishes ([for example, this could be]* lots of photovoltaic panels (with or without storage) or communities which would like to municipalise their wires].

- A DSP’s network operation and development is more linked to incentivised outputs, and therefore their revenues and rate of returns are related to them doing what is wanted of them, [as set out in the PBR mechanism rather than the DSO which sets out their regulatory inputs to do what they want.

- In this way, the DSP is less in control of the development of the network, and is more facilitative of it].

- Finally, it should be fully ‘active’ at all kV levels, and as far as possible between electricity, heat and mobility’.

Both the DSO and DSP above were envisioned as a joint distribution system operation and wires company – meaning that the SO entity and the wires component were together. And the blog also explained why this was the case:

At the moment, a DNO is effectively a joint wires company and system operator. In theory, a DSP could be SO only. The separated distribution wires company would be regulated and would bid in for system provisions, as any other provider. However, that SO portion of the DSP does not, conceptually, have to be formed from the DNO. In other words, the DNO could continue as it is without a SO function. A ‘new’ SO institution could be added to the distribution area. This new ‘platform’ would be regulated to undertake a DER assessment in a dynamic way, and to operate the area most cost-effectively (including via tenders etc) depending on the desired outputs [for example Origami, DeX would produce a platform for social use rather than produce platforms as they usually do for private company use etc]*.

In this situation, this new platform displaces the DNO [but an alternative to this] is the platform [tool] can also be a tool for ‘activating’ the DNOs (ie the platform would not displace the DNO but rather is something that would help turn the DNO into a DSP). This area wide platform would also complement the newly developing private platforms developed by companies like Origami [although would add to issues of regulatory oversight].

There is a clear distinction between an area-wide platform which captures all DER in the area, thereby revealing area value, and working for the public good; and private platforms which work for the best private interests of a company. There is nothing wrong with these private platforms – on the contrary they should be encouraged. However, it is important that there is some form of area market and balancing coordinator to understand what distortions private interests may be injecting into system operation and development, to make sure public policy goals are delivered and that customers do not have to pay to rectify those distortions.

It is remarkable how many people argue that ‘passive’ DNOs are incapable of becoming ‘active’ DSPs however much they are incentivised; and therefore (1) the SO role should be hived off from the wires business; or (2) the DNOs should be re-nationalised.

However, my preference – at least in the short term and unless something changes considerably – is that the wires and SO aspect of the DNOs remain together as they move to a DSP. This is because there should be so much [combined] energy and system activity [ie from EVs, DSR, solar etc] that it should be easier to reveal value if they remain together, [at least for a while]. The GB DNOs may know DER value in a few places in their area which are being piloted but they do not know DER value across their network areas, and therefore they do not understand how that value will change as DER is added. A SO has to understand the area value in order to be able to coordinate and operate it efficiently and it seems easier that they start off combined with the DNO wires in learning that value, and only once the SO ‘knows’ that area based value can they realistically be hived off – otherwise system value remains with the wires company which would not be helpful]*. However, other companies should undertake the non-wires provision and the distribution entity should be regulated with an increasing proportion of their revenues linked to performance based regulation. This regulatory change would not have to happen immediately but the current DNO companies would have to know that, over the next 10 or so years, their regulatory risk is going to change considerably (ie for example 6,5% of additional value of PBR now to say 50% of earnt revenues related to PBR), and that there is a very clear end point of delivering the network aspects of a decarbonised electricity system by 2030.

It may be that it becomes clear that the DNO SO should be separated from the DNO wires company but I think this is a RIIO3 activity – and only once it has become clear what the trade-offs are.

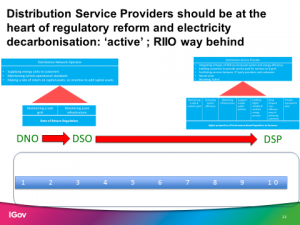

Finally, there was also a figure which argued that the DSO, as I set out, was at about 3 on a continuum of 1 to 10. The DNO was at 1 and a fully functioning DSP, as I set out, would be at 10.

Figure 1 The DNO DSO DSP Continuum

Distribution Entity Understanding Has Moved On

Although I only wrote that blog a few months ago, it seems to me that the discussion of the distribution entity has moved on considerably: this is firstly with respect to the name; secondly, with respect to the functions; and thirdly, with respect to the institutional character or form.

The Name

It does matter what we call these distribution entities with their different functions.

- Firstly, because activating DNOs into active distribution entities is one of two key institutional changes needed to deliver a sustainable, secure and affordable energy system (the second major one being a progressive IISO, although many other changes are also needed).

- Secondly, as the first point above is becoming increasingly accepted, what distribution entities there should be and what their functions should be, and by when, is becoming more widely debated. We need some clear, broadly agreed categorisation of function (preferably across the world) for the distribution entities, and their attendant names, so that we can learn from each other and discuss the merits of one entity versus another.

I am at fault here because IGov changed the NY distribution system provider acronym (DSP) to distribution service provider (DSP) for GB – thereby no doubt adding confusion. I did this because I thought distribution system provider was a too ‘system’ orientated name and I thought the new distribution entity needed a name which implied ‘services’ rather than system and sale; and I also wanted an entity which reflected a combination of energy and system resources (hence service) rather than only system or only energy.

I still would argue that the functions I set out for a DSP above are those that an electricity distribution entity needs to be doing by 2030 in GB if the electricity system is to be decarbonised. I am more open to separating out the DSO operation from the poles and wires entity than I used to be – not because I think it is the right thing to do service-wise, I still think a combined energy and system operation role at the distribution level, given the granularity of data, still makes more sense – but because I am open to questions about whether the DNOs are capable of activating themselves into a market facilitation and coordination activity by 2030, even with the necessary fundamentally different and stronger performance based regulation. If this is the case, then possibly creating a separate poles and wires company and a DSO component may enable change to happen more quickly. If this were the case, then I would expect the DSO to have the same functions as listed for the DSP above, and they would be at 10 on the 1-10 continuum. The only difference would be that they do not have the poles and wires maintenance component.

One could argue that the term distribution system operator (DSO) has become widely used now around the world – but usually DSO is used to denote a distribution entity only responsible for the system operation, market and security aspects. In GB, Ofgem has required the DNOs to deliver DSO plans – and so far WPD and UKPN have done so. In this situation, the DSO is a joint system operator and poles and wires company.

In terms of the name then, the question is whether we should agree to use the term DSO only when we mean a distribution entity which is responsible for system operation, market facilitation and coordination and security – and which is separate from the poles and wires company; or whether a DSO can combine both.

My vote is the former – a DSO would not include poles and wires but it would be a market facilitator, and regulated in new ways. The goal would be to be 10 of the 1-10 continuum above in Figure 1 by 2030 to complement a decarbonised electricity system.

Other names and their functions – DNO, DSP etc. – are not so simple.

Function and Form

Within GB, the ENA Open Networks process has been looking at 5 Future Worlds. All the Worlds have a joint distribution wires and SO company, except for the fifth World, World E, which still has a joint distribution wires and system operation company but it has a separate flexibility coordinator which is situated between the electricity SO (i.e. at the transmission level) and the distribution level. The Government and Ofgem are involved in the Open Networks process, as are 9 DNOs. It has defined a DSO function but obviously all functions remain in the combined wires and SO body so it does not address the name or form problem, nor does it mention timelines for change. This is very much a status quo approach.

A recent 4 blog series by James McGinness, Founding Partner of David Energy based in Brooklyn, New York City has many interesting ideas about the future needs / functions / form etc. of a fit-for-purpose distribution entity, and reading these blogs is well worth persevering with (Blog 1, Blog 2, Blog 3, Blog 4).

A first problem with understanding them is the name problem. There are the usual differences of meaning between DNO, DSO and DSP but with a new acronym to me – TSP (transmission service provider, basically (I think) a transmission wires company). There are other problems in understanding his arguments relating to the differences between US and GB Regulation; the different meanings for certain words – like ESCOs, aggregators, retail markets, utilities etc; and the different assumptions / concepts which come from working in one jurisdiction.

McGunness is also critical of the NY REV. He does say it is the most radical regulatory attempt in the US but he is also worried that the function and form issue have not been sorted out, and that they need to be sorted out, and implemented, soon if the NY REV is to reach its stated goals.

The fundamental argument of his 4 part blog is that we are entering a new phase of distribution liberalisation and ‘the search for a logical retail market’ by which he means (I think, and if I get this wrong then I apologise) a competitive retail market where effectively anyone can buy from anyone and anyone can sell to anyone, and that includes prosumers (including storage) who can both buy and sell. He also means that the distribution entity is separated from the retail (or supply) business – as is generally the case in Europe – and also that the system operation function is separated from the poles and wires functions – and that within these new segments, franchise rights are removed.

McGuiness provides a strong argument for why distribution level markets are necessary, and what their form and functions should be. He argues, and I agree, that the granularity and sheer volume of data when distributed energy resources really get going mean that distribution level coordinating markets are going to be necessary to coordinate all the distribution level information. He makes the argument that only in this way can value for different products be assigned via different markets to be captured via stakeholders and new entrants. He also argues that tariffs (by which he means US regulated tariffs rather than our GB tariffs chosen by each company as they wish (i.e. not a regulated activity excluding the 2 year price cap) will jump start fully functioning, more real time markets. These arguments are well known in Europe, although GB does not have a governance system in place to deliver that value (including not having a process to work out the DER value in the areas). McGuinness argues that NYS also – even within the NY REV which both states that it wants to do that and has a process to do that – is not set up to deliver that value.

McGuiness’s Other Key Arguments about Distribution Form and Function

McGuiness’s four blogs are individually recapped in Blog 2 – so please go to them for details. McGuniness’s key points (from my perspective), relative to the function and form of distribution entities discussion are:

- The poles and wires of the distributed entity should be a separate company (he calls this a distribution service provider DSP (same as the IGov DSP – except the IGov DSP in our view has more or less the opposite function) – they manage the network. He does not say this but it seems to me that he sees this as a low rate of return, low risk type activity – in essence ‘the old’ DNO type activity with input regulation.

- The SO aspect of the distribution utility should become a separate DSO entity – a market facilitator and security deliverer

- 3rd party entities would compete for poles and wires upgrades etc. on the network managed by the DSP; and there would be a non-wire alternative competitive requirement as part of that. He is not clear if the poles and wires company can compete for that work on the poles and wires they manage – but they certainly lose their franchise rights.

- 3rd parties are able to build microgrids / private wires.

- The energy system is bottom-up managed, with transmission as the balancer

- The energy system is moving from economies of scale to one where grid and access (i.e. network charging and access rules) costs dictate which users can access grids and which users do or do not self-organise into firms. Network charging and access rules are central to this ‘modern utility’.

- A modern utility ‘requires a system which handles real time, secure, trust minimised transactions (data) with embedded regulatory oversight and governance, and which does not ‘censor’ users.

- Getting rid of ‘Censorship’, a term he uses to explain how distribution entities control prosumers / customers by the distribution entities deciding on what they can and cannot do, and part of that is by deciding on how much it would cost them to do what they wanted to do (grid access and charging) so that ‘Censorship resistance’ is therefore an important part of regulatory oversight.

- The retail market / supply market is one that enables all customers to buy and sell from whomever they wish.

- Local and coordinating markets are necessary to deal with plethora of data deriving from DER, and to be able to assign value and coordinate cost effectively.

What does this mean for names, form and function of distribution entities?

This leads to a number of issues which have to be decided on.

The DNO-DSO-DSP

Can the current DNO be incentivised to act differently? If this is the case then the combined poles and wire and SO functions can remain together provided regulation is fundamentally different (i.e. moves from input to output regulation). This entity could continue to be called the DSP as IGov talks about it – i.e. a combined wires and system operation company at 10 on the 1-10 continuum above.

If, however, the reality is that DNOs will either not be able to make this leap to their new role or they will take too long to change then their SO function will have to be separated out from them – leading to two distribution entities for each GB area: a DNO and DSO. It seems to me that DNO is a widely understood term as the company running the networks. McGuiness introduces distribution service provider (DSP) for a distribution wires company but, in my view, that adds to confusion so I suggest sticking with the DNO to denote a poles and wire only company.

Alternatively, the current DNO (i.e. joint poles and wires and system operator) can transfer to the lesser role of manager of the poles and wires. They would have a maintenance function but any upgrades etc. would be competitively bid for (organised by the DSO), and this would include NWA.

This would require a new and parallel DSO to be developed / built by a private platform provider. It would certainly be a lot cheaper were it a built platform. But how would this be regulated? Would its assets be even lighter than a separated DSO – or would it be the same? Would there be regulatory issues if the company which built the platform also built multiple other private platforms?

The DSO’s primary operation and market facilitation area has to be under a Grid Supply Point (GSP) – although there could be multiple areas within a DSO area. It is to be expected that these DSO markets will link to other DSOs, depending on what services are offered at what prices. However, the key point is that it is the area under the GSP which reveals value of different DER services. The netting out of markets would happen at the GSP from a bottom-up system operation approach of the area. It makes no sense to have bigger, regional DSOs as a basic unit. They may form from the GSP areas but it is the GSP area as the basic unit which enables the value to be derived.

Regulation

If the DNO is simply a manager of networks, should all the palaver of price controls be part of its regulation? Should it be returned to input based, rate of return regulation? This would be a few percentage points to reflect a low risk business. IGov has long argued against input regulation and finds it difficult to countenance such an idea even for a distribution wires manager, but is open to persuasion otherwise.

If the DSO becomes an asset light, platform business to be incentivised for providing and coordinating data, setting up balancing and coordinating markets, reducing the total infrastructure costs, reducing peak prices for customers, maximising the demand side, complementing a move to digitalised, decarbonised, energy efficient world – then they are going to need progressive, performance based energy regulation.

It also means that the Regulator has to grasp that it has the ability to stop, undermine, channel or enable development. Currently, we as a society, have no way to hold the Regulator to account for its actions.

What is this link between T and D – how far does the SO stretch?

Another issue – given the rapidly changing world – is how to enable whole system thinking and interconnection across T and D, but also across electricity, heat and mobility.

The energy system is currently an asset heavy system rapidly moving to a system with those assets combined with new, big offshore wind farms + interconnectors plus more small scale DER, including storage, and DSR via aggregators – as well as much more decentralised P2P platforms. New connections from EVs, storage and solar etc. are not going to be ‘controllable’ in the past sense. Minimising infrastructure costs and coordinating all of this for the public interest will become far more related to platform and data assets that the current asset base.

DNOs and DSOs will need to be linked to the ESO – and the heat networks. In this world, is it sensible to have individual DSOs linked to the grid supply areas (yes) but individually dealing with the ESO. Should the ESO and all the DSOs become part of one SO? Separating out the SO from the DNOs will cost money – if that is to be done, then possibly the sensible step at that point is to bring them together as one SO. If regulated appropriately, a whole system approach would be taken.

This however seems to work against the greater decentralisation and value of local DER. Maintaining the DSO and the basic units under the GSP seems right. How then is the ESO to interact with the DSOs? Logically, this would see the ESO becoming a balancer.

Where should network charging and access rights be placed?

As McGuiness says, network charging and access is the current means used to ‘censor’ new ways of doing things. There needs to be clarity on principles – and I think this is best in a Strategic Policy Statement (SPS) – but otherwise I think network charging and access rules should be the DSO decision. Moreover, as McGuiness argues ‘censorship’ has to be minimised – this should be incentivised and a new function of the Regulator via its oversight should be to help with that.

Conclusion

Distribution is going to become a much more important aspect of energy system transactions as decarbonisation and digitalisation kick in. This changes energy economics and it opens up new services. It alters roles, and it can be a force for good in energy system transformation. However, the function and form of current distribution entities are not currently fit for purpose for that energy system transformation. Distribution entities will have to be regulated in new ways. They also have to fit the whole system – remembering that the ‘perfect’ way forward for distribution may not be the best for the whole system.

This blog is an attempt to argue for some clarity on the names and functions that are given to different distribution entities. We end up with the DNO to be the poles and wires company (or the next version of the current DNO); the DSO to reflect a separated system operator function from the DNO; and a DSP for a joint poles and wires and SO function which is regulated by PBR.

IGov has hitherto argued for a DSP – and still thinks the arguments of maintaining energy and system together make most sense – but IGov is becoming more open to a DNO and a DSO, if it becomes obvious that the current DNOs are incapable of transferring to a DSP rapidly.

Posted by: HPoulter

Related Posts

« Previous Blog 2 of Name, Form and Function of Distribution Entities Presentation: Issues for GB Energy Policy and the IPCC Next »

{kind=link}