The complex world of price caps – should GB have one, and if so who is eligible?

The complex world of price caps – should GB have one, and if so who is eligible?

Catherine Mitchell, IGov Team, 26th October 2017

Energy price caps have been an important part of the political landscape ever since Ed Milliband announced he would freeze prices in 2013, if the Labour Party was elected at the next election. This ultimately led to a Competition and Mergers Authority Investigation into the Energy Market, and the degree to which it is competitive (please see the IGov website for our multiple submissions to the CMA investigation, kicking off with our first submission and oral evidence here and here). The CMA Final Report was published in 2016, but the argument about how the uncompetitive energy market allows customers to be ‘ripped off’ has rumbled on in the press, becoming ever more political in its nature. A prepayment safeguard tariff was introduced for customers eligible for prepayment meters (about 4 million), coming into effect in 2017 -2020, with a review due in 2019. However, this did not satisfy those involved in the discussion. The Labour Party announced at the 2017 Labour conference that they would cap the average house dual-fuel bill at £1000 (see Table 1 and Figure 1 for its impact). Theresa May announced at the Conservative Party 2017 conference that there would be an extension of the Safeguard price cap, quickly followed by an Ofgem announcement of a Safeguard tariff for about 1 million of those eligible for a Warm House Discount . In parallel, Dieter Helm was asked to undertake an independent cost of energy review, just published and this will be focus of another blog.

Absolute and Relative Price Caps – what are they?

The idea of an absolute price cap is that prices can fall below but cannot rise above a pre-determined threshold. The Labour Party Price Cap of £1000 is an absolute price cap, and the Ofgem Safeguard Tariff would be similar, calculated by a particular methodology. This is different from a relative price cap which regulates the allowed gap between a company’s – or the whole market’s – cheapest and default tariff. The ‘default’ tariff is generally a standard variable tariff (SVT) (as shown below in Table 1 and Figure 1 . An SVT is therefore generally the ‘price to beat’ tariff, so that whilst a supplier may have many tariffs they are usually cheaper (but not always) than the SVT. The SVT continues permanently, unless the customer actively changes it. If a customer switches to a fixed price or fixed term tariff, at the end of that tariff the customer will be ‘rolled’ back on to a SVT by the supplier, unless the customer tells the supplier otherwise.

What ‘harm’ or detriment do SVTs customers suffer?

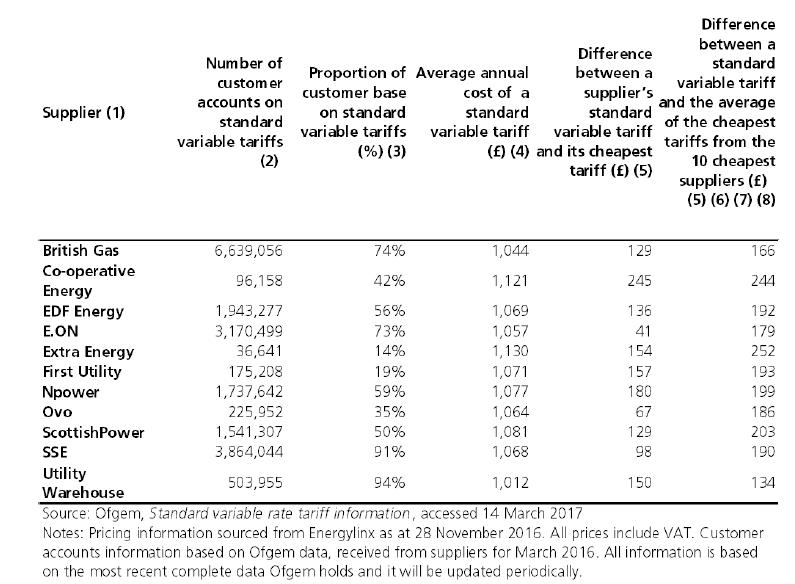

‘Harm’ is an economic term referring to the negative economic impacts of a non-competitive situation. In layperson’s terms, this refers to how much more is an average SVT customer paying because of problems with the energy market? The CMA said that were a prepayment safeguard price cap in place in 2015, the average bill of a prepayment customer would be reduced by £75 a year. The calculation of harm is incredibly complex, and the results vary depending on the different methodologies, but the CMA says ‘between 2012 and 2014, which corresponds more closely to the period over which we have estimated detriment using the direct approach, the central indirect estimate of detriment is around £1.1 billion (of which excess profits earned on domestic customers are around £650 million per year). If we were to use a more stringent efficiency benchmark, the indirect measure of detriment increases to £1.5 billion over the period’ para 201. Table 1 below (and here) shows the difference between the SVT tariffs and the cheapest tariffs offered by 13 suppliers, and these range from the largest difference of Extra Energy at £252, and the smallest with Warehouse at £134. Ofgem found that the gap between the cheapest tariff in the market and the average SVT offered by the Big Six reached nearly £320 in August 2017 (from Ofgem charts).

Who is most affected by this?

The majority of vulnerable customers are on SVTs according to recent Ofgem data: 83% of those living in rented social housing, 75% of those on low incomes, 73% of those with no qualifications and 74% of disabled customers.

What are the basic arguments about price caps?

At root, three broad, but different and / or overlapping, arguments are coming together in the current ultra-political argument about the need or not for a price cap. All support a price cap but have very different views about who should be eligible.

- One is a standard economic view, arguing that the Big 6 suppliers inherited large ‘legacy’ customer bases which either do not switch, or very rarely switch. As a result of this, the Big 6 can charge higher than justified prices to those customers, and then they can use those extra profits to cross-subsidise other tariffs to attract new ‘acquisition’ customers, making it harder for new entrants to develop strong and vibrant new supply companies. It is accepted that for various reasons certain customers are not switching, and until that is enabled some of the most vulnerable of society should have the price of their energy capped.

This view recommends a reasonably limited number of customers be eligible for the price cap – the Competition and Mergers Authority (CMA) recommended those on pre-payment meters (about 4 million, and this was put in place with the Prepayment Safeguard Price Cap); and then Government / Ofgem has just launched a Safeguard Tariff which adds another 1 million of those eligible for a Warm Homes Discount.

- The second view is more consumer-centred and argues that the majority of customers – about 6-7 out of 10 – remain on Standard Variable Tariffs (SVTs) and are paying over the odds. This view argues that whilst customers need to be encouraged to switch, it is not only their responsibility to find the cheapest tariff which suits their needs. This group argues that the Big 6 suppliers should also see their responsibility as providing a ‘fair’ price for all their customers, including their SVT customers (and this de facto means that those suppliers accept they should earn a ‘fair’ profit only). Thus, this group argues, until that occurs there should be a price cap.

There is a much wider spectrum of arguments about who should be eligible for the price cap from this viewpoint – and what sort of price cap that should be. Two well-known commentators reflecting very different numbers of eligibility are: (1) Citizens Advice, who has broadly agreed with a temporary, absolute price cap, but would include all those eligible for prepayment meters (4 million) as well as those eligible for a Warm Homes Discount (2.5 million in all, i.e. 1.5 million more WHD customers than the Ofgem / Government Safeguard Tariff ) – which amounts to 7 million households in total; and (2) John Penrose MP, who supports a price cap for all SVT customers (ie 18 million in total) but supports a temporary but relative price cap. As mentioned above, in this case it is the difference between the lowest tariff offered and the SVT that a supplier provides that is capped. Although a relative price cap (rather than John Penrose’s argument) is supported by a number of smaller suppliers (such as OVO, Octopus Energy and Utility Warehouse) a relative price cap is not widely supported in GB because there are fears that the lowest tariff could gradually become higher, again leading to higher prices of the SVT.

- The third view is a combination of the previous two, and is represented in particular by Martin Cave, a member of the CMA Energy Market Review team. Professor Cave dissented from the main CMA report recommendations (pages p 1415-1417), arguing that whilst he supported the CMA work and analysis, he did not think the CMA recommendations were strong enough given that the level of harm on customers. However, the difference in his arguments to the CMA is twofold – that imposing a temporary and absolute price cap would improve the competitiveness of the energy markets, and improve the efficiency of the Big 6 suppliers themselves; and secondly, that waiting for improvements via switching etc. would take too long.

Professor Cave argued that more should be done for all customers on a SVT tariff by implementing a temporary price cap on all SVT customers not on a prepayment meter (14 million) in addition to those eligible for a prepayment meter (4 million) thereby leading to about 18 million on a price cap for two years. Those 14 million non-prepayment households represented 59% of all domestic non-prepayment customers at April 2017 or 64% (18 million) of all domestic customers when including prepayment.

How many customers are there on SVTs?

Ofgem produces a very handy guide to SVT numbers, although it should also be noted this is a very geeky and confusing area. In total, there are around 28 million electricity and 21 million gas meter points in Great Britain, with about 26 million domestic accounts. Many of these households take their gas and electricity from the same supplier, with on average 70% of electricity customers, and 80% of gas customers, having dual fuel accounts. As of October 2016, around 18 million domestic energy accounts (14 million paying by non-prepayment methods) are on SVTs. Broadly, 6-7 out of 10 households remain on SVTs. While there has been more switching (the term used for customers moving from one supplier to another) both in total numbers (which could be the same people) and in total households, still the vast proportion of customers have never switched; and will not do so for decades based on current rates, if ever.

How many of these SVT customers do the Big 6 have, and how big is the difference between their lowest tariff and SVT?

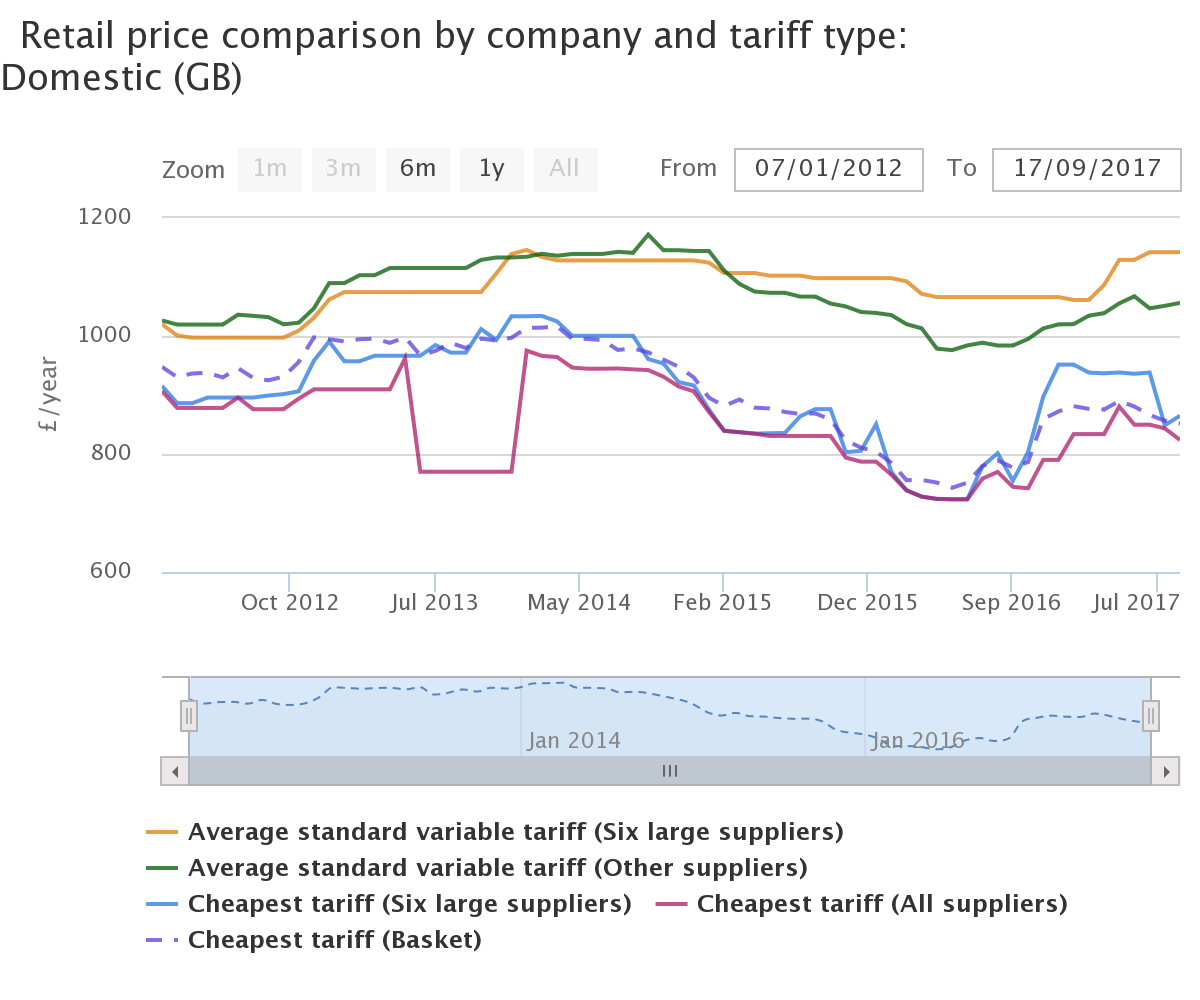

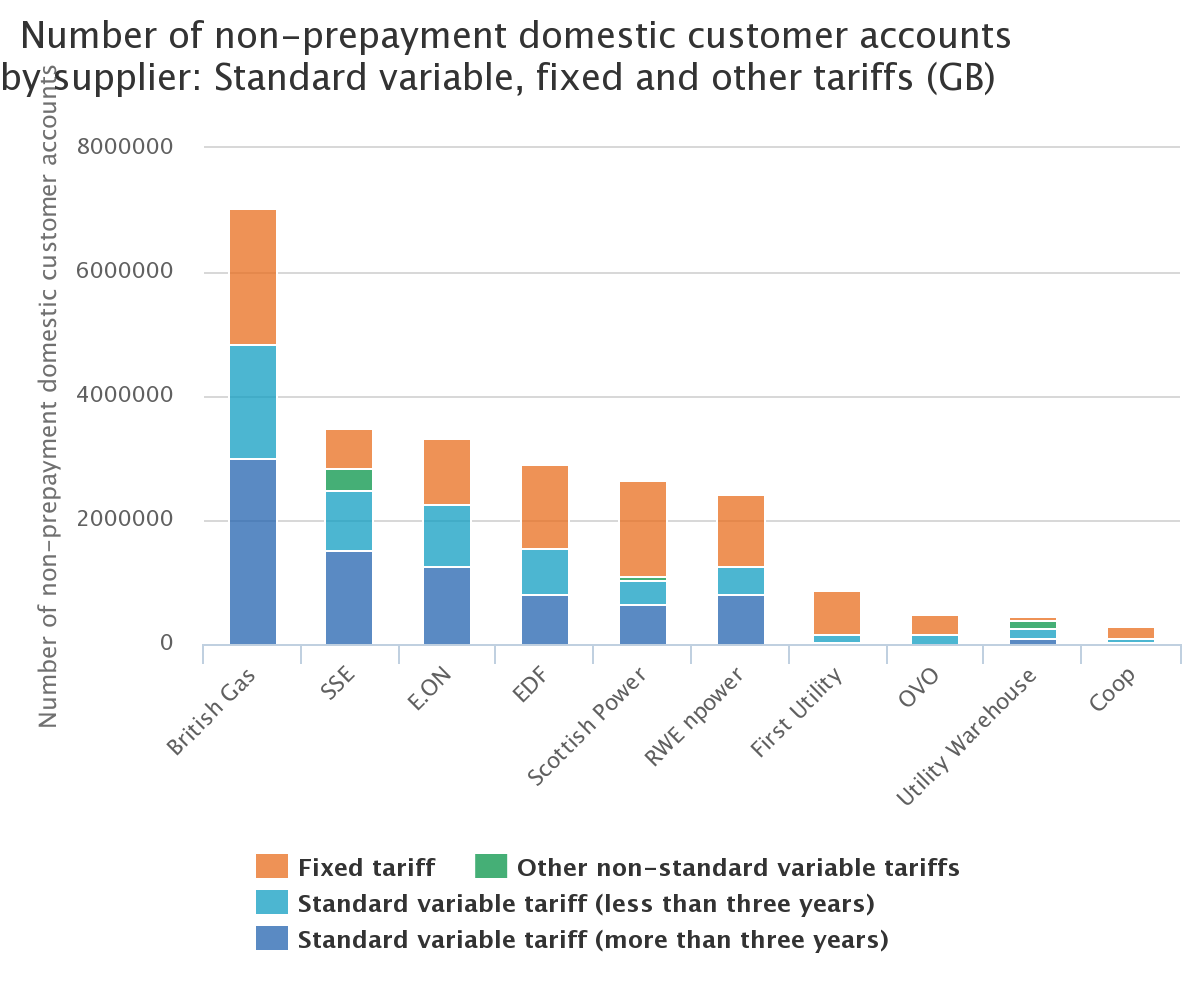

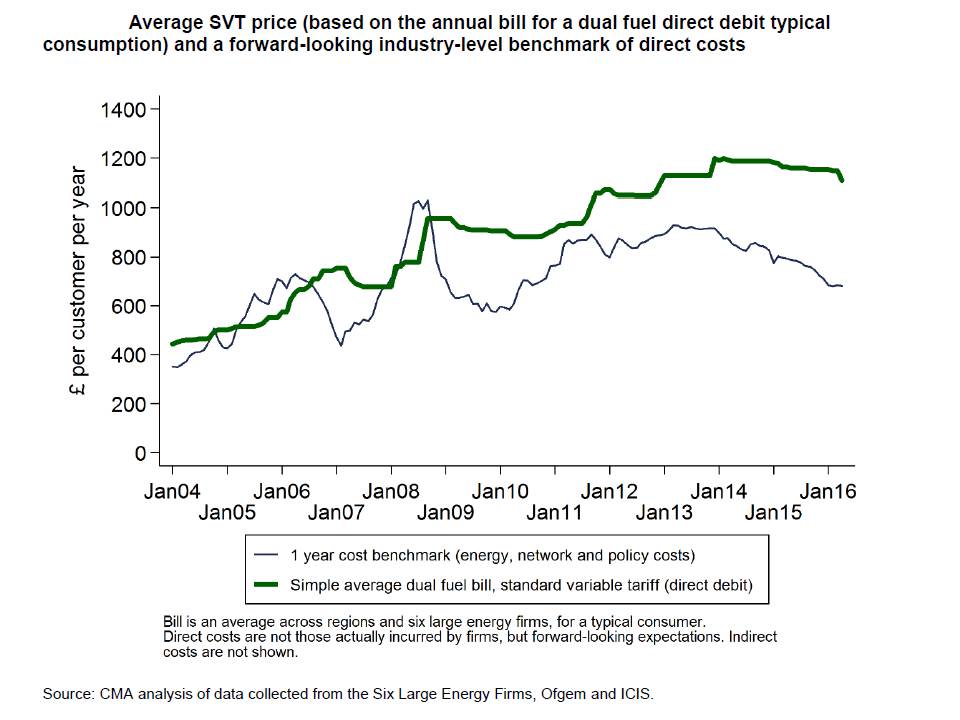

The House of Commons Library has produced a very useful debate pack on energy prices (March 2017) and it shows how many SVT customers each of the bigger suppliers have and the difference in their tariffs (taken from an Ofgem report). Figure 1 shows this as an average of Big 6 suppliers versus other suppliers over time. The Big 6 also dominate the SVT market (Figure 2), also shown in the Ofgem retail market indicator report.

Table 1 Supplier SVT Total Numbers; Proportions; and Price Differences With Other Tariffs

Figure 1 Supplier differences over time. Source: Ofgem

Figure 2 SVT proportions of customers by Big 6 and other suppliers

What has happened to the price of energy over time?

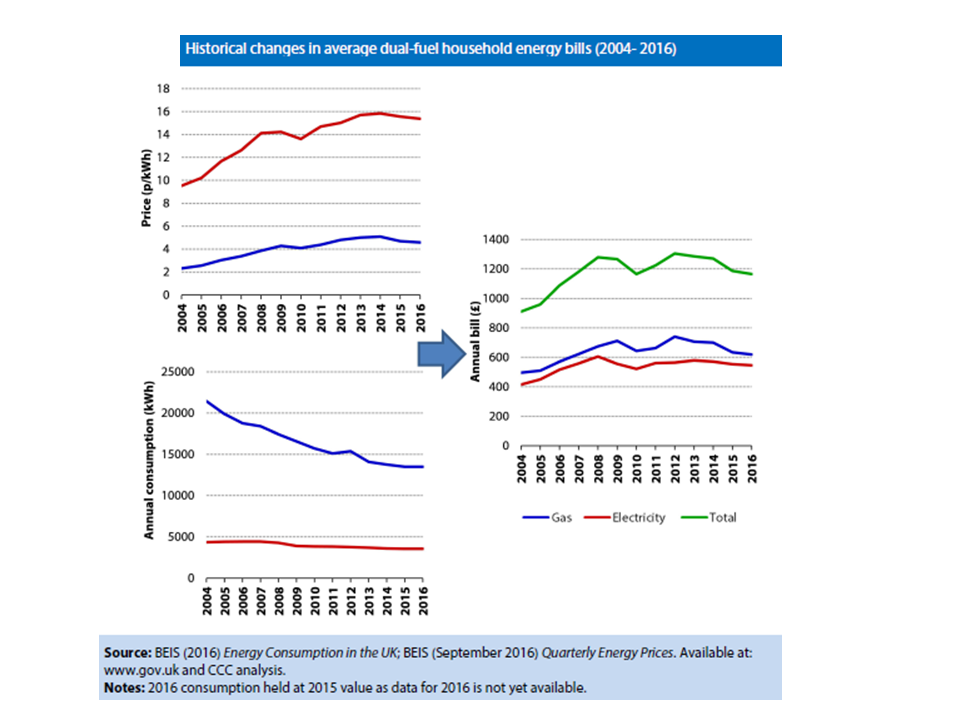

Gas and electricity SVT prices have increased over time, see The House of Commons Energy Price and CMA for Figure 3 below, and CCC for Figure 4. But domestic prices for gas or electricity are not high relative to other European countries – the UK coming somewhere in the middle (although gas prices are higher than electricity; and industrial prices are high). The CCC (Figure 4) is showing that prices would be higher, were it not for improvements in energy efficiency.

Figure 3 The Price of Gas and Electricity Over time

Figure 4 Changes in average dual fuel household prices, consumption and bills. Source: The CCC

Have the Big 6 profits been excessive?

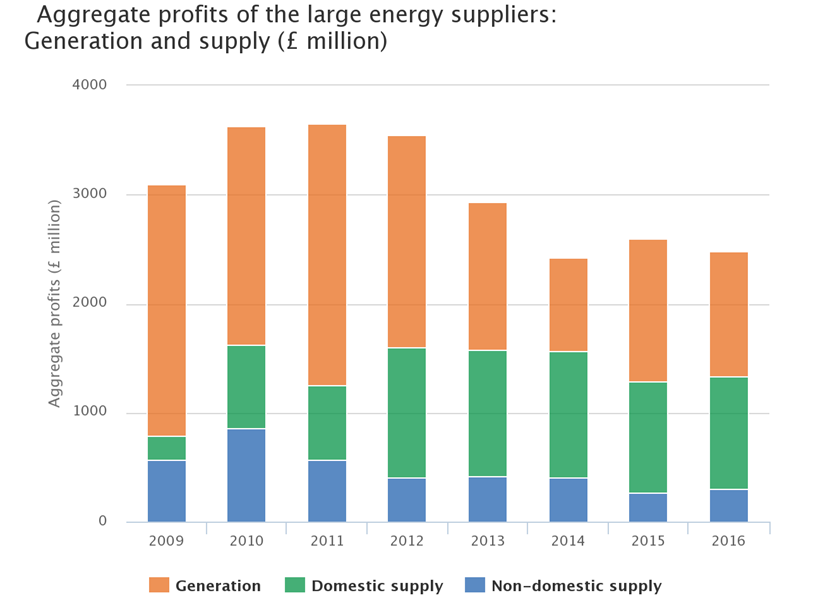

This is an area where there is a certain amount of information (see Ofgem; CCC;) but information needs to be more detailed, meaning examining the levels of profit for each supplier for each tariff. In that way we could see what profit was being made on SVT customers, but also the extent to which the profits from those customers were being used to cross-subsidise other tariffs, or the gain new customers. The Big 6 have made large profits in terms of the total amount from aggregate generation and supply (as shown in Figure 5 below): it is now about £2.5 billion pounds, down from its highest level of £3.6 or so in 2011.

Figure 5 Aggregate Profits of Large Energy Suppliers (£m)

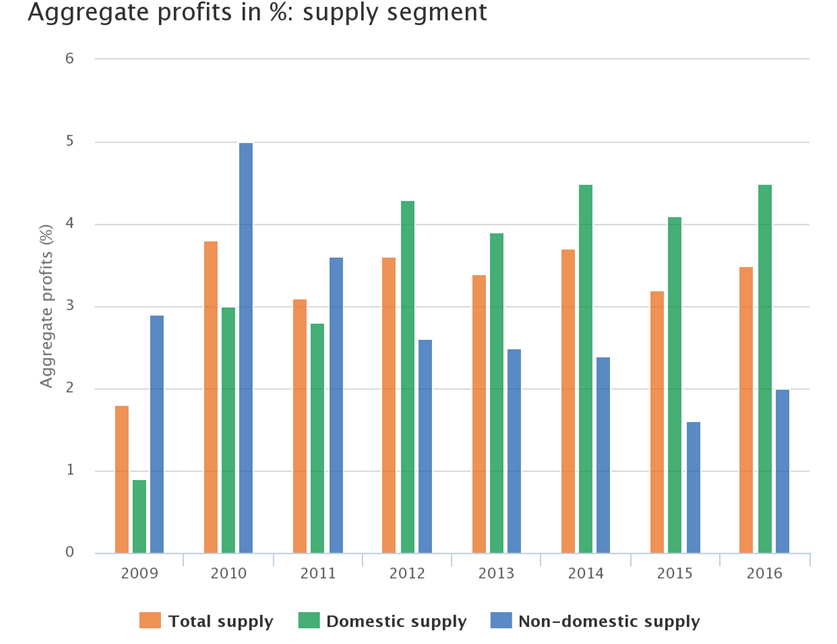

However, this is only about 2-4.5% in aggregate profits (as shown here, and in Figure 6 below), and not a high amount relative to other private companies, and even compared to energy monopolies (see here, here and here about DNOs).

The issue that needs to be got to the bottom of, and then published, is not these average % profits but the % profits from the SVT customers for each supplier – and this is harder to discover. The CMA showed that the Big Six earned on average 11% (for electricity) and 15% (for gas) more per kWh from customers on SVTs.

Another argument is that the profits are excessive in the context of falling input costs of energy (Figures 4 and 5). Energy prices have increased in real terms since 2000 by more than 75% for electricity and more than 125% for gas though the increase wasn’t always steady. The Committee on Climate Change also reported rises in prices, but because they relate to a slightly longer period the figures are a little different: a 98% increase in gas prices and 61% increase in electricity prices, between 2004 and 2016. Over the long-term period, the increase in prices is even starker.

Figure 6 Aggregate Profits of Large Suppliers in %.

Are the Big 6 suppliers the key culprit in high energy bills?

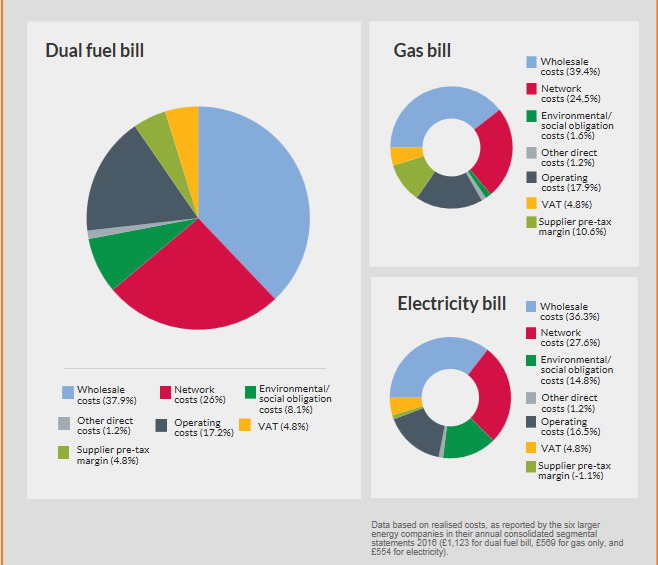

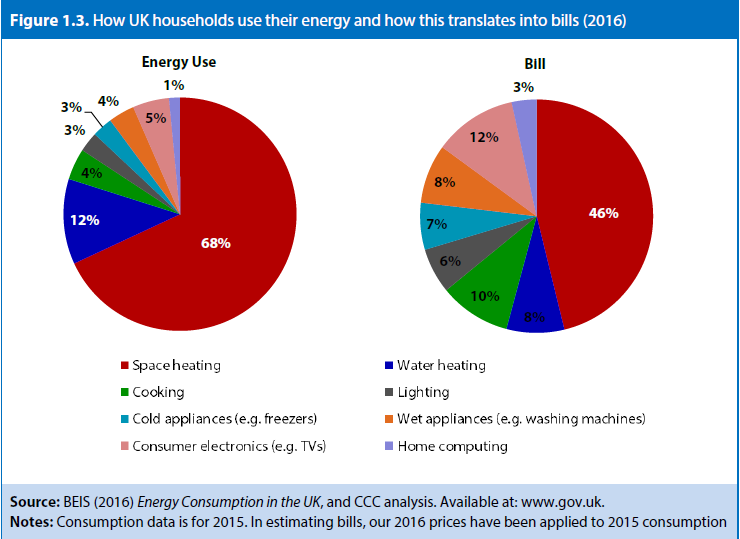

Figures 7 and 8 below show the constituent costs of energy bills, and the link between what households use energy for and their bills. Clearly, suppliers are charging more to SVT customers than others. However, network companies are making greater profits than suppliers (see here, here and here about electricity DNOs). One could point the figure at numerous institutions for this failure. Government has for reasons which few understand trapped GB into a 35 year contract for Hinkley Point C – thereby increasing the environmental and social portion of the price – whilst making limited in-roads into household energy efficiency. As the CCC shows in Figure 4, it is energy efficiency of appliances and domestic buildings which bring down bills, because an energy efficient home leads to buying less energy. If Government were really serious about high energy bills, they would put in place an energy efficiency policy which met with the customer proposition – meaning that the policy would be designed in ways that meant that customers would become involved. This has short term costs within the price, but leading to permanent benefits for bills.

Figure 7 Breakdown of Energy Bills . Source: Ofgem

Figure 8 Household energy use and relation to bills. Source: The CCC

Conclusion

As the above points illuminate – price caps are a contentious and complicated aspect of energy policy. There is experience of price caps around in GB and the world, some good and some bad. The US States routinely have a ‘default’ tariff – a permanent tariff (equivalent of the SVT), which is the price to beat within that State for other tariffs (if there is retail competition) and it is a regulated price calculated by the State Regulator. Denmark has a default tariff for heat. And there are many more successful examples.

It is clear that the Big 6 are able to use their SVT customers to charge higher prices; it is also clear despite years of effort that the majority of those SVT customers are not switching – and some customers may be happy with their supplier. Nevertheless, it is also clear that the majority of vulnerable customers are those with a SVT tariff. My view is that there is no doubt that there should be some sort of default tariff for those customers, meaning prepayment meter customers and those on the WHD.

I have more of a problem with a straight price cap for all SVT customers (i.e. the difference for the 6.5 million and all 18 million SVT). The problem with setting it by price is that it ignores wider public policy of moving to a sustainable (i.e. decarbonised and energy efficient) energy system.

My preference for these SVT customers would either be:

- A default tariff that would be linked to a rising block tariff (RBT). In other words, as a customer uses more energy, the price of that energy would go up in blocks. It seems to me if GB does go down this big step towards intervention, then it should link it to public policy goals of encouraging energy efficiency. Since Ofgem is able to undertake this methodology of assessing the ‘price to beat’ then I think it should be able to do this with a RBT, as occurs in California for example. In theory, it should also be possible to help the vulnerable – they could get a certain amount of kWhs free etc. (as in Belgium) before the RBT kicks in. This default RBT would be temporary, but up for review.

Or

- A one-off levy (again up for review) on the Big 6 suppliers, or in proportion to numbers of SVT across all suppliers over a certain size. This levy would go directly to a revolving, zero interest loan fund. Discussion of who should be eligible for those funds should be up for discussion. Certainly domestic customers and local authorities for social housing.

Posted by: Iain Soutar

Related Posts

« Previous Global Insight 17 – 24th Oct 2017 New Thinking: On Professor Helm’s political economy Next »

{kind=link}