AUSTRALIA

Tesla big battery proves it’s worth

The Tesla big battery in South Australia, the Hornsdale Power Reserve, is a 100MW/129MWh battery. In the first quarter of this year it has proven its worth in the Frequency Control Ancillary Services (FCAS) market by showing its speed and accuracy, in comparison to a conventional large steam turbine, to respond to frequency control events. This speed is also being recognised in the battery’s ability to respond to major faults in the system. The Australian Energy Market Operator (AEMO) is expecting to use batteries in its new System Integrity Protection Scheme (SIPS) mechanism.

SIPS will use battery technology to act as an interim power source in response to a major fault. It is expected that the speed that the batteries can react to such an event will provide a ‘stop-gap’ whilst slower moving conventional power systems come online. This will prevent load shedding and the possible risk of blackout, as happened in South Australia in 2016.

It is the multiple applications for battery technology that is making AEMO look at modifying the electricity market rules to give value for these possible multiple income streams.

ARENA announces second large VPP in South Australia

The Australian Renewable Energy Agency have announced that they will be investing $7.8m toward a $30m virtual power plant (VPP) development in South Australia. This will be the second large-scale VPP in the state after the SA government/Tesla announcement earlier this year. This second VPP, located in Adelaide, will offer subsidised battery storage to home owners. The VPP will incorporate the Decentralised Energy Exchange (DeX) platform, which will allow the VPP to sell services to the networks and the energy market via a digital marketplace. This will be the first commercial venture for the DeX platform.

USA

Solar fight continues in the US

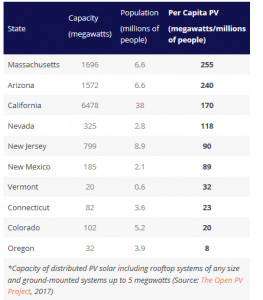

US States continue to press for governance which enables solar development. Some are successful (for example the cap on solar numbers in South Carolina has been removed) and some find it stubbornly difficult to move on. New business models (BMs) are developing and it is becoming clearer that BMs such as Third Party Ownership have been successful in terms of deployment, although less beneficial in terms in local involvement.

A new transmission line for New York State?

The New York Power Authority has petitioned state regulators for authority to rebuild the Moses-Adirondack transmission lines in Northern New York, which run 86 miles, built in 1942 and have exceeded their service life.

Licensing and engineering studies will continue through 2019, with NYPA planning construction for a start in 2020 and be completed by 2023.

If approved by the Public Service Commission, the project will increase the lines’ voltage capabilities from 230 kV to 345 kV, allowing more renewable energy from upstate New York to be connected to the state’s power system.

Energy efficiency and solar keeping costs down in New England

ISO New England released a draft of its 10-year forecast saying increasing amounts of energy efficiency and rooftop solar will trim power usage and peak demand over the coming decade.

The draft report said that without the growth of efficiency and solar, the region will likely see a compound annual growth rate of energy usage by 0.9%, or 142,488 GWh in 2018 to 154,364 GWh in 2027. But after factoring in efficiency and solar, the grid operator estimates that net energy usage will drop 0.9%.

For peak demand, the draft report estimates summer peak demand will rise in a compound annual growth rate of 0.8% without the mitigation of efficiency and solar. But again, once those are factored in, summer peak demand is projected to fall by roughly 0.4%.

EUROPE

New German government faces challenges in regaining climate leadership

After the lengthy formation of the new government critics have suggested that the coalition treaty lacks the ambition and detail needed to reinstate Germany as a climate pioneer. The distribution of costs of the Energiewende remains fiercely debated and Germany is set to miss self-imposed and European emissions reduction goals. Added to these challenges the country’s political landscape has undergone significant changes with the right-wing nationalist party AfD becoming Germany’s third biggest political force. The AfD are the first German party to openly question the existence of man-made climate change and actively promote an anti-energy transition position.

However the new environment minister, Svenja Schulze, highlighted the need for Germany to restore its role as a climate pioneer in her first address to parliament suggesting this will be achieved through a joint effort between the government and the country’s industrial companies. The national Climate Protection Law, due to be introduced in 2019, will be a key tool in accelerating emission reductions and is expected to detail binding measures across electricity, heat and transport to ensure Germany reaches its 2030 climate target.

German ‘meta-study’ calls for greater analysis of the relationship between decentralization and the need for power grid expansion

Researchers at Germany’s Öko-Institut have published a review of the need for new power lines in a renewable electricity system. Findings highlight that a more nuanced understanding of the relationship between decentralisation and grid expansion is required which considers both decentralised flexibility and generation, as well as the influence of market models on grid requirements. Grid congestion happens locally but current market models are based on national price signals. One route to addressing this is the adoption of nodal pricing where the grid is broken up into sub-grids or “nodes,” each with its own prices. In reviewing nodal pricing the study finds that larger (more centralized) zones are easier to manage; with smaller, more distributed, zones increasing the cost of power generation and flexibility options. However the study found difficulty in comparing costs as there are no agreed assessment criteria for calculating all the costs and land requirements (for electricity generation plants, flexibility options and infrastructures). The study also notes that nodal prices are unlikely to happen quickly as they would require fundamental changes to the EU market model and integration.

Storage developments

European ambitions on energy storage continue to develop. The Danish government is planning to spend €17.5m on supporting large scale energy storage projects that are close to market. Shell have said they want to bid for some of the funding to set up a hydrogen electrolysis facility. EDF has set a goal of developing 10GW of storage around the world by 2035 in a new Electricity Storage Plan, which would triple its current portfolio. Part of the anticipated market will be the residential battery systems in France and Europe, and Africa is also a priority market, where it wants to serve 1.2 million off-grid customers by 2035. Meanwhile The Energy Collective has a good summary of the seven new gigawatt-scale battery factories due to open across Europe by 2020, which will eventually produce 80GWh a year of lithium-ion batteries, more than three times the current global capacity.

Coalition presses for Dutch ban on central heating boilers from 2021

A coalition including boiler manufacturers and installers, environmental groups and energy sector associations in Holland are calling for sales of conventional gas boilers to be banned from January 2021. From that date, households would be required to fit some combination of a heat pump, solar heating or a hybrid boiler-heat pump system or connect to a district heating system. However, it is estimated that even hybrid systems are three times more expensive than conventional boilers at the moment, and so a new loan system is also being proposed. The idea of the coalition is that this measure will feed into the plan for the new Climate and Energy Agreement due this summer, and follows a commitment from the Minister of Economic Affairs and Climate Change, Eric Wiebes, to look at how to phase out gas boilers.

WIDER GLOBE

BNEF –Falling Costs for Solar, Wind and Storage

Bloomberg have published the headline conclusions of their most recent analysis on the levelized costs of electricity (LCOE) from renewable technologies and storage. The research found that in the first half of 2018, the benchmark global LCOE for onshore wind is $55 per megawatt-hour, down 18% from the first six months of 2017 and for offshore wind at $118/MWh, down 5%. While solar PV without tracking systems is $70 per MWh, down 18%. The report found that lowest costs for onshore wind were found in Australia, Brazil, India and Sweden and for PC in Australia, Chile, India and Jordan. BNEF is now showing costs of onshore wind of just $39 per MWh, down 46% on a year ago, and for solar PV at $41, down 45%. By comparison, coal comes in at $68 per MWh, and combined-cycle gas at $93.

BNEF also noted that the costs of storage are continuing to decrease with lithium-ion battery price index shows a fall from $1,000 per kWh in 2010 to $209 per kWh in 2017 and note that ‘The conclusions are chilling for the fossil fuel sector’.

Global Coal Plant Completions Fall for 2nd year in a row

A coalition of environmental groups have published an assessment of the global commissioning and completion of coal plants which shows a 28% drop in the start-up of new coal plants over the last year and given the fall last year, this has led to a 41% decline since 2015. Over the same time periods, the decline in construction starts has been 29% and 73%. This fall has been experienced globally but in particular in the major coal constructors such as China, where in 2015 60 GW of new capacity was opening and only 34 GW in 2017, while in India 21 GW started in 2015, but only 9GW in 2017. In China, due to overcapacity on the grid in 2017 the central government began suspending hundreds of coal projects, with 98 GW shelved in January and 93 GW in September (and 21 GW of overlap). In India although 152 GW of coal power capacity was added from 2006 to 2017, all of the 6,920 MW that started construction in 2017 was sponsored by state owned entities with public funding, the report suggests that the falling costs of renewables are now deterring private sector finance for coal. The draft 2016 National Electricity Plan calls for rising demand to be met with 275 GW total renewable energy capacity by 2027, with no coal plants needed beyond those under construction.

Posted by: HPoulter

Related Posts

« Previous Global Insights: 27th March 2018 Event Report: Innovation & Governance for Future Energy Systems Next »

{kind=link}